We recently received an inquiry from a reader asking, “Is the first-time homebuyer tax credit still available?”

Unfortunately, the answer is no. The first-time homebuyer tax credit has been expired for several years.

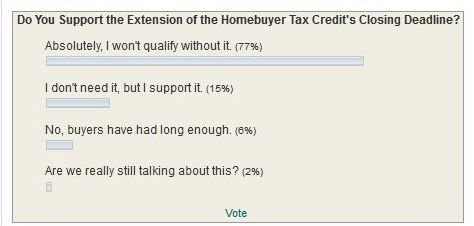

Overwhelming support for an extension

While the tax credit has been expired since 2010, there was overwhelming support among HSH.com readers to extend the deadline. Here is the results from a poll we ran back in 2010:

First-time homebuyer programs

While the first-time homebuyer tax credit is expired, there are state-sponsored homebuyer assistance programs geared toward first-time homebuyers. Each state has specific programs headed up by their housing finance agencies that offer some sort of home buying assistance.

HSH.com has compiled a database of statewide first-time homebuyer programs. In addition to first-time buyers, states may also offer assistance to repeat buyers, veterans, the disabled, teachers and first responders. Most states have more than one program targeted at homebuyers.

It’s important to understand that each state offers different and unique programs, and the specific programs have different parameters as to who can qualify, how to qualify and what the particular benefits are.

Many state-run housing assistance programs have no set expiration date, rather they expire when the money allocated to the particular effort runs out -- many are first come, first serve.

In all 50 states, a first-time homebuyer is defined as "someone who has never owned a home or hasn’t been a homeowner in the last three years."