Awaiting Confirmation Or Rebuttal

May 10, 2024 -- It's well understood that the inflation data over the first few months of 2024 hasn't been good and caused investors to do a full re-think of expectations for interest rate cuts by the Federal Reserve. Still, there remains at least some optimism that a rate cut or two is yet in the cards for this year, but what's now needed is confirmation as to whether price pressures are holding steady, increasing still or starting to subside.

We do get a fresh slew of inflation information next week, as monthly updates to the Producer and Consumer Price Indexes are due, plus a updates on import and export costs. The Fed of course follows these indicators to help determine the direction of inflation, but prefers to track a core measure derived from Personal Consumption Expenditure (PCE) data. Core CPI inflation has been running around 0.9% to 1% above core PCE, but right now, and in terms of the potential for change in Fed policy this year, it's less about the level of inflation than the direction in which it's headed.

Annualized core CPI has been edging downward in stutter steps over the last six months, posting a cadence of 4%, 4%, 3.9%, 3.9%, 3.8%, 3.8% over that time. Another small step downward in April wouldn't change the near-term interest rate picture all that much, but would improve the chances that July or certainly September opportunities might be back "in play." Futures markets currently place virtually zero chance of a June lowering of rates, but there is at present about a 25% chance of a July move and a 63% probability of a quarter-point cut come September.

Should the new inflation data prove less favorable than hoped, the odds of a change in rates would diminish, and bond yields and mortgage rates might firm anew.

|

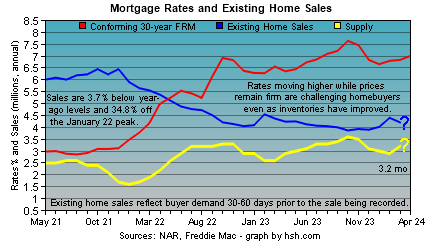

While measurably below the worst levels of last year, mortgage rates are still plenty high, and the housing market is pretty stagnant as a result. We're now just about in the heart of the spring homebuying season, and while sales of existing homes will likely improve a bit yet this spring due to beneficial seasonal effects, but as home prices and mortgage rates are well above year-ago levels, it seems very unlikely that they will best even the modest marks set then. The availability of existing homes to buy is improving somewhat, as inventory levels this March were 14.4% higher than a year ago, but more homes available to buy isn't especially helpful if home affordability is still falling.

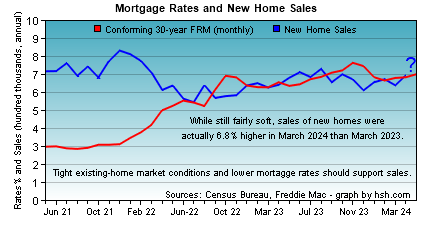

The new construction market is less impacted by adverse conditions, as there is plenty of inventory available to buy, and builders may be able to subsidize financing or offer price discounts to help improve affordability for buyers. However, new construction often isn't a direct substitute for existing homes, since much large-scale construction takes place far outside center cities and inner suburban circles, potentially adding commuting considerations and more into the home purchase calculation. Still, new homes are a viable option for some folks, and homebuyers who have had difficulty participating in the existing home market over the last few years appear to be warming up to the chance to buy and own a home even if it means more time in the car and a less-established neighborhood experience.

|

A couple of weeks ago, we took a broader and deeper look at What's holding back housing? this spring. Lower mortgage rates would of course help, but there are a number of intertwined components that need to move in sync to impart real change, and some of these are more intractable than others.

Want to get MarketTrends as soon as it's published on Friday? Get it via email -- subscribe here!

As we follow the ebb and flow of consumer credit, we have wondered in recent months why it appears that so little actual consumer borrowing seems to be taking place. Consumer credit balances at the nation's banks expanded by just $6.3 billion in March, another month that came in well below expectations (of a $15b increase, in this case). Revolving credit balances (usually credit cards) balances increased by just $0.2 billion; this was the slightest increase seen since the last "pandemic stimulus paydown" month almost three years ago.

Some consumers are probably using up savings to continue to fuel purchases and so not using credit. However, it's also true that borrowing conditions for credit cards have tightened, both in terms of higher interest rates and tighter underwriting standards; this may also be impacting their use. One other factor we hadn't really contemplated as a factor could be the considerable growth of the "Buy Now, Pay Later" (BNPL) method of purchasing goods. It may be that BNPL offers are being utilized in place of some credit cards transactions, so revolving balances would be lower as a result. Overall, the debt to the consumer is the same but the borrowing isn't reflected in the Fed's long-running Consumer Credit series.

The other component of the Consumer Credit report covers installment-type (non-revolving) borrowing. Comprised of things like auto, personal and education loans, this component too is burbling along at a low level and has been for some time. The muted pace of growth in outstanding balances here is most likely due to the effects of the cancellation of billion of dollars of student loan debt. In March, non-revolving credit balances rose by just $6.1 billion, most likely due to a modest uptick in auto sales in the last month of the first quarter of 2024.

Find these only at HSH.com!

As noted, tighter credit conditions probably play a role in consumer borrowing behavior. The latest Senior Loan Officer Opinion Survey covering the second quarter of 2024 showed a general ongoing tightening of credit card conditions but somewhat less imposition on other kinds of consumer borrowing. For the most part, the report noted that lending standards were largely unchanged for conforming and government backed mortgages, but slightly more restrictive for the kinds of mortgages that end up in lender portfolios. These include loans that don't fit the Qualified Mortgage definition, Jumbos, ARMs and similar less-easily-salable mortgage loans.

Applications for mortgage credit rose by 2.6% in the week ending May 3, according to the Mortgage Bankers Association. Request for credit to purchase homes picked up by 1.8%, erasing a decline the week prior, while applications to refinance existing home loans expanded by 4.5%. It was the first increase for both of these segments in a couple of weeks, likely from folks who simply can no longer wait for lower rates to move forward with home purchases or refinances. Without a measurable retreat for mortgage rates, sustained increase in mortgage applications remain unlikely.

The labor market remains tight, but is thought to be coming into "better balance", per the Fed's characterization. Reported weekly, initial claims for unemployment assistance are one high-frequency indicator of change in the labor market and so bear watching. There was a flare in new applications for unemployment benefits in the week ending May 3, when 231,000 folks put in requests for assistance. While not an outsized number in any historical context, it was a jump of 22,000 for the week, the largest bump since January, and one that put the current level of initial claims at a level not seen in more than eight months. Is this a blip, or the start of a softer pattern in labor markets? We'll have to wait to see.

With plenty of troubles in the headlines and inflation stubborn, it's little wonder that consumers have got the blues again. The preliminary reading of Consumer Sentiment for May by the University of Michigan showed a darker demeanor to start the month, as the headline index here retreated 9.8 points to 67.4, a six-month low. Current conditions were assessed to be less favorable, posting a 10.2-point fall to 68.8 in the initial review, while expectations for future conditions also retreated, falling 9.5 points to 66.5 to start May. Consumers polled by the survey also now expect inflation to run at a 3.5% clip over the next year, up from 3.2% and the highest expectation since November; the five-year inflation outlook also edged up to a six-month high of 3.1%. Although not "unanchored", expectations for inflation certainly also aren't heading in the direction the Fed would prefer to see, either.

See today's mortgage rates every day at HSH.com

Does mortgage history repeat? Usually. Find out what happened last week/month/year with MarketTrends archives!

We learned from the twin ISM reports last week that both the manufacturing and service sectors of the economy ran at a sub-par rate in April, and we know that a drawdown of inventories was part of the reason that first quarter GDP came in at a muted level. Data that covers stockpiles at the nation's wholesalers in March confirmed this, as holdings of goods fell by 0.2% for the month, making it declines in two of the first three months of the year. For March, wholesaler holdings of durable goods shrank by 0.1%, while non-durable inventories dropped by 1.1%. These depletions came despite a 1.3% slump in sales; even so, there is still about 1.35 months of goods on hand relative to their current pace. As such, wholesalers probably don't need to place much by way of new orders to factories to keep enough stock handy, and so the sluggish pace for manufacturing activity seems likely to continue.

Mortgage borrowers, investors and others continue to pore over the incoming data in hopes that there will be just enough softness in economic growth, just enough loosening in labor conditions and just enough easing of price pressures to allow the Fed to gain confidence again that inflation is headed to their 2% goal, much as they had at the end of 2023. Evidence of all of these things has been scant, but a few signs of such may be starting to appear. The sub-par readings from the ISM and softer-than-expected hiring in April, a first-quarter GDP that was rather below the recent trend, the small kick in unemployment claims and others may or may not be signals of a change in the pattern. Certainly, there have been data head-fakes before.

Current Adjustable Rate Mortgage (ARM) Indexes

| Index | For The Week Ending | Year Ago | |

|---|---|---|---|

| May 03 | Apr 05 | May 05 | |

| 6-Mo. TCM | 5.43% | 5.34% | 5.09% |

| 1-Yr. TCM | 5.19% | 5.04% | 4.72% |

| 3-Yr. TCM | 4.76% | 4.50% | 3.64% |

| 10-Yr. TCM | 4.61% | 4.35% | 3.44% |

| Federal Cost of Funds |

3.893% | 3.889% | 3.239% |

| 30-day SOFR (daily value) | 5.32541% | 5.32901% | 4.82369% |

| Moving Treasury Average (MTA/12-MAT) |

5.153% | 5.114% | 3.977% |

| Freddie Mac 30-yr FRM |

7.22% | 6.88% | 6.35% |

| Historical ARM Index Data | |||

Is a softer tenor for the economy the precursor to getting inflation moving in the right direction again? It's too soon to say, but to be more certain that they are (or rebut these indications) confirmation will be needed. This could start as soon as next week, and as far as mortgage borrowers are concerned any improvement in borrowing costs can't come soon enough.

Next week sees a busier calendar of economic data, but the bulk of it doesn't start to come until the middle of the week. This means that this week's pretty flat trend in the yields that influence mortgage rates should be able to hold for at least the early part of the week, We think when Freddie Mac reports next Thursday at noon, the average offered rate for a conforming 30-year fixed-rate mortgage will hold just about steady, with a decline of a couple-few basis points the most likely outcome.

What's the outlook for mortgage rates for much of the spring homebuying season? See what we think when you take look at our latest Two-Month Forecast for mortgage rates, covering April into early June.

To start each year, we release our Annual Mortgage and Housing Market Outlook. In it, we take a forward look at a range of topics, including mortgage rates, Fed policy, home sales, home prices and lots more; come July, we do an interim review of our expectations. Have a look and see if you think we're off or on point with our long-range forecast.

For a really long-run outlook, you'll want to check out "Federal Reserve Policy and Mortgage Rate Cycles".

Have you seen HSH in the news lately?

Want to comment on this Market Trends? -- send your feedback, argue with us, or just tell us what you think.

See what's happening at HSH.com -- get the latest news, advice and more! Follow us on Twitter.

For further Information, inquiries, or comment: Keith T. Gumbinger, Vice President

Copyright 2024, HSH® Associates, Financial Publishers. All rights reserved.