What is HARP and do I qualify for a HARP loan?

The Home Affordable Refinance Program (HARP) was a federal refinance program targeting underwater homeowners. First announced in March 2009, HARP is designed for homeowners who are current on their mortgage payments, but who haven't been able to refinance because they have limited equity, no equity or negative equity in their homes.

The Home Affordable Refinance Program (HARP) was a federal refinance program targeting underwater homeowners. First announced in March 2009, HARP is designed for homeowners who are current on their mortgage payments, but who haven't been able to refinance because they have limited equity, no equity or negative equity in their homes.

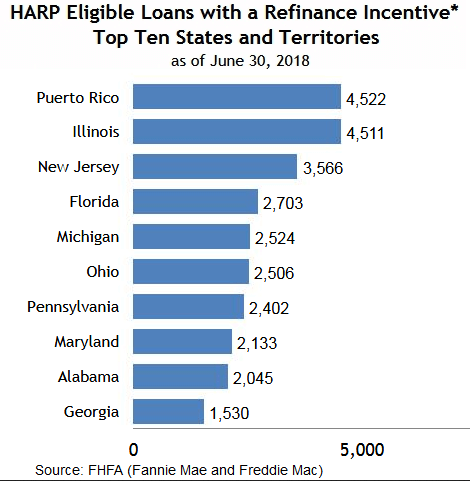

The Federal Housing Finance Agency (FHFA) and the Treasury Department originally estimated that four to five million borrowers would be able to refinance under HARP. Since the program began, almost 3.5 million homeowners have refinanced their homes through HARP, according to the latest statistics from HUD. Given present conditions, it is estimated that fewer than 38,000 U.S. households might still benefit from participating in the program. More than 70% of these eligible homeowners reside in 10 states.

On August 17, 2017, the FHFA announced that the HARP program would be extended again, and will now run until December 31, 2018. At the same time, HARP's replacement, the Streamline Refinance program will also run concurrently, starting with loans originated on or after October 1, 2017.

Note: The HARP program expired on December 31, 2018.

Do I qualify for HARP?

A HARP loan looks a lot like any other mortgage. Since HARP mortgages are backed by Fannie Mae and Freddie Mac, the underwriting process will resemble that of any other conventional mortgage. There will be loan disclosures to sign and supporting financial documentation to remit. Mortgage lenders are looking for borrowers with solid incomes, good assets and quality credit scores.

Here is the full list of HARP requirements:

- The mortgage must be owned or guaranteed by Fannie Mae or Freddie Mac

- The mortgage must have been sold to Fannie Mae or Freddie Mac on or before May 31, 2009

- Borrowers must be current on their mortgage payments with no payments more than 30 days late in the last six months and no more than one late payment in the last 12 months

- Eligible property types are primary residence, one-unit second home and one-to-four-unit rental property

- The current loan-to-value (LTV) ratio must be at least 80 percent. There is no maximum LTV limit for a new fixed-rate mortgage. The maximum LTV for a new adjustable-rate mortgage is 105 percent.

- You cannot have previously refinanced under HARP (unless it was a Fannie Mae loan refinanced under HARP between March and May 2009)

5 ways to prepare for a HARP refinance

Once you determine that you qualify for HARP, it’s time to start preparing your finances. Here are five ways to prepare for a HARP refinance:

1. Ensure Fannie or Freddie backs your mortgage

Fannie Mae and Freddie Mac each have a loan lookup tool which allows homeowners to search for their loan:

To check if your mortgage is backed by Fannie Mae, visit https://yourhome.fanniemae.com/calculators-tools/loan-lookup. If your mortgage is not found, try Freddie Mac's loan lookup at https://myhome.freddiemac.com/resources/loanlookup.

Mortgages not listed on either website are not backed by Fannie Mae or Freddie Mac and, therefore, are not HARP-eligible.

2. Determine if your mortgage is old enough

Only those whose mortgages were securitized prior to June 1, 2009 can apply for HARP. In general, this means that your mortgage must have started in mid-May 2009 or earlier. You can find your mortgage start date by looking at your closing paperwork.

Note: Since it can take up to 60 days to securitize a Fannie Mae or Freddie Mac loan, even if your start date is close to June 1, 2009, you still may be ineligible.

3. Does your mortgage have mortgage insurance?

HARP is designed to help homeowners with or without private mortgage insurance (PMI) and lender-paid mortgage insurance (LPMI). The general rule of thumb is that if you have mortgage insurance, your new HARP mortgage must have the same level of coverage.

Some borrowers have been denied a HARP refinance because of LPMI. If your currently lender won’t refinance because of LPMI, shop around for one that will.

4. You must be current

HARP requires that all homeowners have made their last six mortgage payments on time, with a maximum of one 30-day late payment in the past year. This information is verified against your credit report, so be sure to review your credit reports prior to submitting your HARP application.

5. Organize your HARP paperwork

Since HARP mortgages are underwritten like every other type of mortgage, you will be required to provide bank statements, a driver's license, homeowners insurance information, pay stubs and W-2s. If you're self-employed, you'll have to provide a few years of tax returns to verify your income.

The speed in which you return these items to your lender can dictate your mortgage rate. If you're going to apply, you must follow these tips to be approved and to close as quickly as possible.

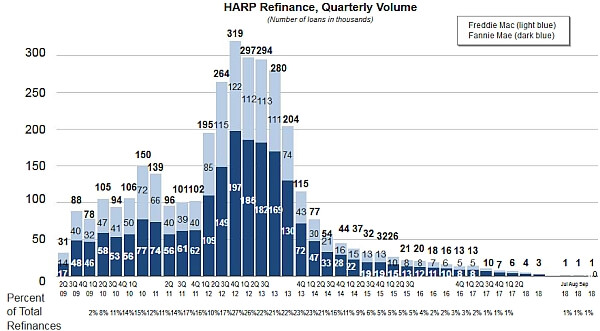

HARP Refinance Trends 2009-2018

Why don’t I qualify for HARP?

While the HARP program has evolved over the years to allow more borrowers to qualify, there are still several reasons why you wouldn’t qualify for HARP, including:

- Bad credit. Some borrowers can't qualify due to impaired credit or too many late payments on their existing mortgage.

- Equity issues. HARP has no maximum LTV ratio for borrowers who obtain a new fixed-rate mortgage, a maximum LTV ratio of 105 percent for borrowers who get a new adjustable-rate mortgage, and a minimum LTV ratio of 80 percent for all loan types. However, lenders typically impose their own guidelines, called "overlays," which may include different LTV rules.

- No re-HARPs. Homeowners can only utilize the HARP program once.

- Fannie and Freddie. You will not qualify for HARP if your mortgage is not owned or guaranteed by Fannie Mae or Freddie Mac.

FHFA Senior Policy Analyst Michelle Murphy says borrowers who've previously been denied for HARP should try again and shop around.

"Call your current lender and share with them that you want to explore a HARP refinance," she says. "If you're denied, find out the reason and don't be discouraged. You may be able to refinance with another lender."

Can I refinance a first and second mortgage through HARP?

In order to refinance both a first and second mortgage through HARP, you must meet two additional requirements, according to MakingHomeAffordable.gov:

- The lender that holds the second mortgage must agree to remain in junior lien position

- You must be able to meet the new payment terms of the first lien mortgage, and demonstrate your ability to do so

Can I refinance a rental property through HARP?

The general answer is "yes," you can refinance a property under HARP if it is a rental. Of course, the loan must still meet all the typical HARP requirements.

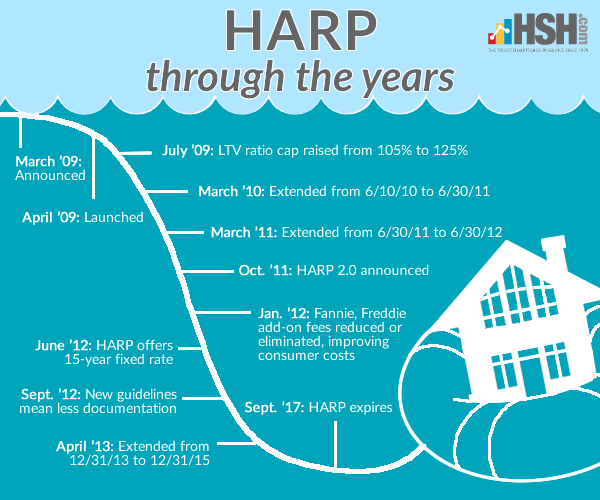

HARP Timeline

Since 2009, there have been many changes and updates to the HARP program. Here are some of the most important changes to HARP since the program began:

(Image: HSH.com)

Am I eligible for HARP 2.0 despite my recent bankruptcy?

According to Fannie Mae, they have removed the "requirement that the borrower (on the new loan) meet the standard waiting period and re-establishment of credit criteria in the Selling Guide following a bankruptcy or foreclosure. The requirement that the original loan must have met the bankruptcy and foreclosure policies in effect at the time the loan was originated is also being removed.”

This indicates that you should be eligible. Freddie Mac usually follows the same policies as Fannie Mae, but there may be some differences.

(Keith Gumbinger, Dan Green and Marcie Geffner contributed to this article.)

(Image: KHL49/iStock)

Related content:

How to refinance when you are self-employed

Refinancing? Use this document check list

Refinance calculator: The best way to finance your refinance