Are you a financial slacker? If so, you're not alone.

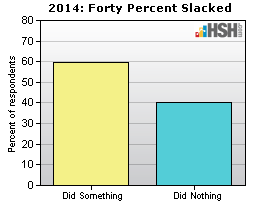

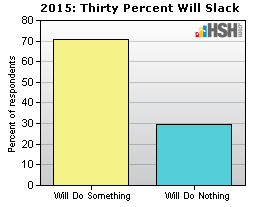

A recent HSH.com survey of 1,906 U.S. adults found that 40 percent of respondents hadn't refinanced or prepaid a mortgage, saved more for retirement, paid off credit-card debt or tried to boost a credit score in 2014, and 30 percent had no intention of taking those actions in 2015.

What's more, only about 39 percent of the survey respondents said they'd taken even one action, even with so many on the list from which to choose.

Analysis paralysis

Why were people so disinclined to improve their financial situation?

True, some folks don't have a mortgage or credit-card debt and are already retired or saving plenty toward that goal. But those people aren't typical.

One reason people don't act is what PJ Wallin, founder and lead adviser at Atlas Financial, a financial planning firm in Richmond, Virginia, calls "analysis paralysis."

"Some people are perfectionists," Wallin says. "It's hard for them to get started."

Many people know they should save for their children's education, their own retirement and an emergency fund, for example. But which of those is the top priority and how much should be allocated to each? Trying too hard to resolve that puzzle can prevent even conscientious people from moving forward, Wallin suggests.

Missed mortgage opportunities

Another cause of inaction is a "set it and forget it" mindset, Wallin says.

Another cause of inaction is a "set it and forget it" mindset, Wallin says.

This pitfall might explain why some people opted not to refinance to lower their payment because their current payment was manageable or they were in wait-and-see mode, hoping their home would appreciate so they could refinance at 80-percent equity and without mortgage insurance.

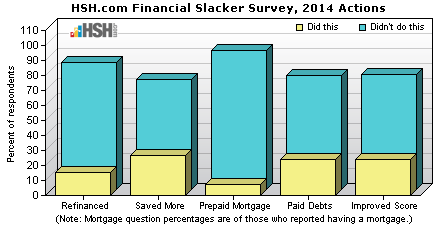

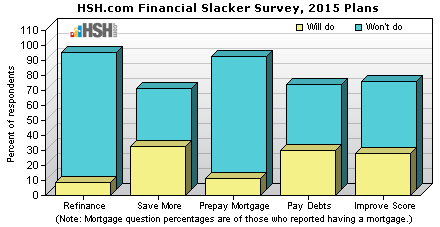

Only 15 percent of the 825 in the HSH.com survey who said they had a mortgage had refinanced in 2014. Even fewer -- just 9 percent -- said they intended to refinance in 2015, despite the fact that mortgage rates are expected to remain quite favorable for much of the year.

Moreover, only 3 percent said they'd prepaid a portion of their home loan in 2014 and just slightly more than 11 percent said they planned to prepay some of their mortgage in 2015.

Mental laziness can also lead to inactivity, says Ronit Rogoszinski, wealth adviser at Arch Financial Group, a financial planning and investment firm in Long Island, New York.

"Unless people are sophisticated enough or willing to actually look at the number and savings they will have over time, they seem to take an attitude of: 'It's so much bother and what's the point?'" she says.

That sort of unexamined thinking can stop people from refinancing or saving more for retirement, Rogoszinski says. Rather than increase their investments steadily over time, they try to time the markets, waiting for the next buying opportunity, which they then miss and continue to wait.

"When the downturn comes, they're busy or they didn't listen to the (financial) news that day, then they wake up three months later and say, 'I missed it again,'" Rogoszinski says.

Financial peer pressure

So what motivates slackers to take action to improve their financial situation?

Peer pressure, often in the form of cocktail party chatter, can be one factor.

"You hear somebody else did it and you think maybe you should think about doing it, too," Wallin says. "That's a common theme."

Education and awareness can prompt action, too, Rogoszinski suggests. As people become better informed, taking even small steps can be a way to start.

"A willingness to at least try to do the right things even if, financially, it's not enough to make a point is still getting the habits in place so when the dollars can be more substantial, the habits are already there," she says.

Celebrate personal financial wins

Alan Moore, a certified financial planner at Serenity Financial Consulting in Milwaukee, Wisconsin, says people who want to improve their financial situation need to figure out what motivates them to achieve their other goals and apply those insights to their finances.

Whether that's an accountability group, friendly wager or other approach, the point is to "recognize your weaknesses and strengths and use that to find out what works for you," Moore says.

It's also important not let naysayers turn modest on-the-road-to-success achievements into negatives.

"Societally and culturally, we have a problem celebrating wins. That holds us back because we accomplish a few things and there's no one to celebrate with. When we get a small win, we think, 'I have so much more to do,'" Moore says. "Ultimately, every step matters."