You want to become a landlord! Great choice, not least because that role can provide you with exceptional flexibility. You could:

- Buy just one or two homes -- ultimately, perhaps, to provide yourself with an additional income through retirement, or acquire lots of units and become a full-time landlord

- Do all the work yourself -- From fixing a leaky toilet or broken HVAC unit to being your own unqualified lawyer and accountant, or do none of the work yourself -- and pay others to do it for you

- Develop a hybrid model that lets you do some work yourself but delegate things you're no good at to professionals

- Keep your operations local -- or spread your property empire across the state or country

- Specialize in high-end rentals for upper-middle-class renters -- or serve poorer communities with affordable housing

If you want to be a landlord, you're going to be faced with a wealth of opportunities and choices. And some of those you probably won't even have thought of. So this guide is intended to help you through the decision tree that faces all existing and new landlords. But first ...

Find mortgages for investment property

When you shouldn't become a landlord

Let's get this out the way. There's no point in sugarcoating it: not everyone should be a landlord.

To start with, it takes an entrepreneurial spirit and a certain appetite for risk. After all, there's no such thing as a 100%-safe investment. And, whether you're borrowing money or using your own resources, you're going to be putting some serious sums on the line. Losses can and do happen.

What it takes to be a landlord

In addition to nerves of steel, you're likely to need a whole lot of other skills. And few people have the whole package -- business and real estate knowledge, repair and maintenance expertise and people skills.

Practical skills

Most new landlords have no choice but to do much or all of the work themselves. They have mortgage payments to make and can't afford to waste cash on paying others to do work they can do themselves.

That can involve having (or quickly acquiring) a comprehensive range of home improvement skills: from plumbing and decorating to carpentry -- and from yard work and gutter-cleaning to roof repairs. Of course, you'll have to hire a professional if safety is at stake. But you'll likely want (need) to do everything you possibly can when you begin -- even if that means calling an emergency plumber or turning out at 2 a.m. to repair a burst pipe.

Interpersonal skills

Besides being handy with a hammer, you'll also need some marketing and interpersonal skills. You're going to have to work out how to find new tenants -- and then vet them to exclude deadbeats, vandals and those who want to use your property as a base for criminal enterprises.

Once you've selected tenants, you'll want to build a relationship. If you're lucky, you'll barely see them. But expect at least some to require a lot of attention. You may have to:

- Chase the rent, by phone and email and in-person

- Field complaints from tenants

- Field complaints about tenants from neighbors or other tenants

You could find yourself facing a scary person who is behind on the rent, plays loud music at all hours and is probably dealing drugs out of your building. How do you feel about that prospect?

Professional skills

Then there's the business side of being a landlord. You may be entering and ending legal relationships regularly. And, occasionally, you may need to evict a tenant. Will you use an attorney or do the legal work yourself? At the same time, there's going to be a pile of the city, state and federal regulations to observe.

Equally, you're going to want to stay on top of your bookkeeping and minimize your tax -- while staying on the right side of the IRS. Again, will an accountant do that or you?

Catch-22

There's often a Catch-22 in play here. Your need to use your own practical, interpersonal and professional skills is usually greatest when those skills are least developed. It's when you're a new landlord that every penny counts most. After a few years, finances typically get easier. And it's then you're least capable of performing tasks yourself.

So we've just identified the single most important skill a landlord needs: to learn quickly on the job. And that means enjoying the process.

Related: How to Buy a Home as an Investment Property

A good time to become a landlord?

Now that you know how difficult it is to be a landlord, it's time to explain why you'd want to bother.

You're still reading! That's great. So far, we've been trying to weed out those wannabes who fondly imagine that the life of a landlord means just collecting rent checks from the mail box.

So let's look at the other side: why now may be a good time to become a landlord.

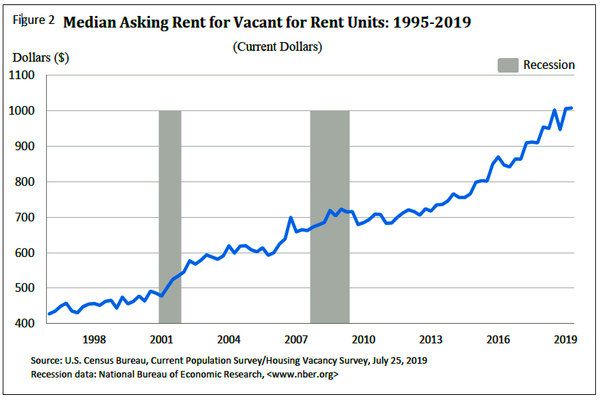

Maybe the biggest plus is the sheer number of Americans who are renting their homes. In 2016, 36.6% of all heads of households in the US were renting, according to a Pew Research Center survey. There had been a big rise in that percentage over the previous decade. And the proportion of renters was the highest it's been since at least 1965 -- more than half a century earlier.

A chart from the US Census Bureau shows how median rents have climbed, partly as a result of the extra demand:

Small wonder 71% of investment property owners reckon now's a good time to buy, according to the National Association of Realtors® (NAR) Investment & Vacation Home Buyers 2018 study. However, rent growth has slowed somewhat this year nationwide.

Getting started

Have you ever been in one of those blue-skies-thinking meetings where your boss promises that no idea is too stupid to say out loud and nobody will laugh at anyone else's suggestions? Bosses lie, too.

But, when you're considering being a landlord, it's not a bad idea to clear your mind of preconceptions and think the unthinkable. And, as long as you keep your dreams to yourself, nobody's going to laugh at you.

Yes, you'll have to scale back those dreams later, in the face of reality. But let your imagination run wild until you have an idea of what you want from your new venture. And try to get to a point where you can answer some basic questions:

- Who? To whom do you want to rent? Upscale professionals, young families, students, companies?

- What? Individual apartments or whole blocks or buildings? Single-family homes in suburbia? Condos?

- When? Do you have the resources to go ahead now? Or will you need time to get your finances and credit in order?

- Where? Downtown? Suburbia? Rural locations? Near where you live? In your state? Elsewhere?

- Why? What is your goal? A modest retirement nest egg? To be your own boss? To get rich?

You may not yet have the answer to most of those. And that's fine. But perhaps your vision is beginning to come together.

Related: How to Get a Mortgage for Investment Property?

Choosing a rental property

If you have never been a landlord before, your financing options are likely to be limited. You should get preapproved for financing before you go shopping for rentals. There is no point in looking for property you can't finance. While the property income plays a big part in your loan approval, your down payment amount is another constraint that will probably limit how much you can spend.

Another catch-22

The problem many new landlords face is that most mortgage programs require previous landlord experience. So if you need experience to get an investment property mortgage, but you can't get that experience without buying rental property, that's a problem. But there are several solutions.

Back door rental

One way to get around the requirements of buying a rental is not to buy a rental. That is, buy a new primary residence instead. You can purchase a new home for yourself and face much more lenient mortgage requirements: smaller down payment, easier guidelines -- and rent out your current home to get your landlord experience.

Property management company

Some lenders will consider an inexperienced landlord if he or she engages the services of a property management company. These outfits charge 10% to 40% of your gross rents, depending on the property location and type of rental. Long-term rentals get the lowest rates, while vacation rentals charge at the high end because turnover is so frequent.

Property management companies perform much of the administrative work for you. Every once in a while, you get a statement showing your vacancy rate and detailing what's been spent on:

- Repairs and maintenance

- Finding and vetting new tenants

- Renovations between tenancies

- Insurance premiums

- Where appropriate, property taxes and homeowners' association fees

- Dispute resolution

- Attorney's fees

- Management company's fees

And, with luck, you should get a nice check with that statement. You've little to worry about. You're paying the management company to ensure you remain compliant with all local, state and federal laws and regulations governing rental properties. And it will collect rents and chase arrears.

Meanwhile, you're probably paying an accountant to keep the IRS happy. So your main roles are to field the odd call from one of the company's managers who has a query or some new information -- and to bank those checks. Nowadays, even the banking can happen automatically.

Multi-unit property

Most government-backed loans are only for primary residences. But there is an exception: both FHA and VA home loan programs allow you to purchase a duplex, triplex or fourplex, and live in one of the units. You can finance it with just 3.5% down (FHA) or 0% down (VA).

Both programs set higher loan limits for multi-unit properties than they do for single unit properties, and allow you to count 75% of the gross rents as income when underwriting your loan.

If there are no existing tenants or leases in place, lenders order a special appraisal with a rental schedule on it. The appraiser determines what the property would reasonably rent for, and the lender usually accepts that.

Running the numbers

When you buy investment property, you use your head, not your heart. That means running the numbers and making objective decisions. Note that the property condition is a factor, and you'll need to consider an individual property's expected maintenance and repair costs in the expenses to make an accurate comparison.

There are many ways to evaluate the financial prospects of a rental property. Whatever metric you choose, use it consistently to compare properties and choose the best deal.

We'll summarize a few popular ones here.

Net operating income, or NOI, is your bottom line: the total income the property generates (after all expenses), not including debt service costs (loan costs).

Cash flow accounts for loan costs. To determine the cash flow, simply subtract the total expenses (including debt service) from total income. If a property has a rental rate of $1,000/month ($12,000 annually), and $6,000 in annual expenses, then the investment property's annual cash flow will be $6,000, which is a positive cash flow.

Cap rate, or capitalization is considered the most "pure" metric. That's because it only evaluates the property, not the financing. It takes into account vacancy, credit losses, other income, and operating expenses. It gives you a rate of return for your investment. Cap Rate = (Cash Flow/Property's Value) x 100.

Cash on cash (COC) tells you how long it will take to recover your initial investment with the annual before-tax cash flow. Cash on Cash Return = (Cash Flow/Cash Invested) x 100. Divide your total cash investment by the annual cash flow to get a rate of return. If a building costs $250,00 down and after annual loan costs delivers $25,000 of cash flow, your COC is 10%. In ten years, your property would earn enough to cover your initial investment.

Should you buy a fixer-upper?

You have choices when shopping for rental property. You can go with new units in pristine condition, which reduce the repair and maintenance, get you higher rents and generally come with fewer hassles. But they are more expensive. Expect cap rates to be lower for these properties.

Class A properties are most desirable for tenants, but not always for investors.

Class A properties are most desirable for tenants, but not always for investors.

On the other hand, many investors like Class B and Class C properties because the right ones can be upgraded and improved to Class B+ or Class A status. It depends on their location and the local rental market. If rents in a Class A neighborhood are rising sharply, improving a nearby Class B property could vault it to Class A status and pay off nicely. That is why it pays to study local rental markets before buying.

Class A properties

- Highest quality buildings in their market

- Less than 15 years old

- Most desired amenities

- High-income earning tenants

- Low vacancy rates

- Convenient location

- Professionally managed

- Highest rent

- Little or no deferred maintenance issues

Class B properties

- Older than A class properties

- Higher vacancy rates than A class properties

- Present an opportunity to add value by improving

- Can be acquired at higher cap rates than A class properties

- Are close to schools and amenities

- Look nice but need updating

- Have no health or safety issues

- Good neighborhoods

C-class properties

- Located further away from schools and amenities

- Older than 20 years

- Less-desirable neighborhoods

- Less-affluent tenants

- Higher vacancy rates

- Need extensive repairs and upgrades to move up in class

For many investors, Class B is the "sweet spot" because they are less risky than Class C and because you can achieve a higher rate of return than with Class A properties. When you have more experience in picking out and renovating property, Class C becomes more doable if that's the direction you'd like to take.

Related: Tips for Buying Distressed Properties

Financing when you buy a rental property

That NAR study revealed another startling fact: 42% of those property investors paid for their purchases in cash, meaning without a mortgage. There's a good reason for that: borrowing to pay for investment properties is generally much tougher than borrowing to buy your own home.

Low or zero down payments

The only real exception to that is when you take a government-backed loan for a block comprising two to four residential units. But you must occupy one of those units and rent out the other(s). With the Federal Housing Administration (FHA loan) and the Department for Veterans Affairs (VA loan), you can make a small (3.5% for FHA) or zero (for VA) down payment. Those both have relatively relaxed credit standards, too.

But they also have a downside:

- You can only have one such mortgage at a time. That's because you have to live in there, and you can't live in two places at once

- These programs are not intended for the most expensive properties on the block. There are loan amount limits

- FHA loans require mortgage insurance, no matter how much money you put down. There is both an upfront premium (currently at 1.75% of the loan amount) and a monthly premium, which never drops off

However, these can be a great way to get started as a landlord. Lenders fear that newbies have no idea what they're getting into and that their ventures will crash and burn. But a couple of successful years as a landlord of a three- or four-unit block can give you credibility and make you look an attractive bet when you apply for a conventional (not government-backed) mortgage.

Conventional mortgages for landlords

If you don't want a VA or FHA loan to buy rental property, it's nearly impossible to become a landlord without a pile of savings -- or a rich backer or partner. To start with, you'll need a 20% down payment for each of your first five acquisitions, rising to 25% after that.

But that's just the start. You must usually document cash reserves to cover six months of mortgage payments. And that applies to your own home, too.

So if you own your own home and want to buy your first rental property, you'll need enough cash for your down payment and closing costs, plus savings to cover six months of payments on both home loans.

Making it full time

Many successful landlords fly by the seats of their pants. They seem to operate wholly on instinct. Whether they really are doing that or just like giving that impression will no doubt vary from individual to individual.

But one thing's for sure. You can improve your chances of success by careful planning. To be a landlord is to be a businessperson. And that should mean having a business plan.

A business plan is how you scale your vision from the desirable to the doable. By all means, maintain your dreams. But break down the practical steps you'll need to take to achieve them.

So your plan may cover decades. But it's the first five years -- and especially the first three -- on which you'll focus.

Why a business plan?

A proper business plan can be an exceptionally valuable tool for an entrepreneur. But it can be absolutely essential if you want to borrow money or attract an investor.

For you, a plan lets you set goals and establish milestones. Those allow you to measure your progress toward achieving those goals. If you're falling short, you'll have the tools to identify why. And you might be able to get yourself back on track or reset your objectives.

For a lender, a plan's even more important. Especially as a new landlord, you're going to have a lot to prove. And a business plan shows you're a serious player who's thought through every aspect of your enterprise. In other words, you're a better bet as a borrower or investment than seats-of-their-pants landlords.

What's in a business plan?

The National Federation of Independent Businesses recommends that your business plan comprises at least seven sections:

1. Executive summary -- your chance to sell your venture in a couple of pages. Provide a compelling snapshot of your plans or nobody's going to bother reading the rest of the document. Write this first section last

2. Company overview -- identify your venture's legal status (sole proprietorship, limited liability company, partnership, limited liability partnership, etc.) and provide some background, including how long you've been trading, past financial figures, products (rental homes), and short- and long-term goals. It's fine to say you're a startup if you are

3. Products and services -- you're renting homes, which are both product and service. Describe the sorts of homes (inexpensive apartments, say, or suburban single-family ones or whatever) you plan to specialize in and why you've chosen that specialization. Or say you'll create a diverse portfolio

4. Market analysis -- show you've researched your market and understand it. Your market is your prospective tenants, so they're people who want to live in the sorts of homes you're offering in the places you own them. You need to know your area's rents and real estate price trends, vacancy rates and any costs specific to the neighborhood -- such as special assessments, higher-than-usual crime, or community recreation fees.

5. Strategy and implementation -- explore your plans to attract and select new tenants, retaining the good ones and discarding the troublesome ones. Show you have a realistic appreciation of costs, including your vacancy rate (times when a unit has no tenants) and what you'll have to pay for maintenance and repairs. Include legal, accounting and other professional fees.

6. Organization and management team -- this may be just you. Say so. If your dad's a retired contractor and is going to do much of the maintenance work, say that, too. He's a big asset. Many lenders and investors see the person or people who are borrowing as more important than the product. So sell yourself here. Emphasize any relevant experience, qualifications and achievements

7. Financial plan and projections -- after your executive summary, the financial section may be the most important of all. If you're already in business, provide your recent financial history. Otherwise, move straight into your plans and projections. You'll need the following forecasts for the next five years: cash flow statements, income statements, balance sheets and capital expenditure budgets

Yes, those financial documents will necessarily be based on assumptions. But we'll get onto those next ...

Assumptions

All business plans are based on assumptions. You can't know the future for sure so all you can do is make guesses about it. But, in any business document, those guesses must be sensible and informed. Yes, they can lean toward optimism. But not too far.

When you're writing your business plan, imagine you're sitting across a desk from a hard-nosed loan officer or investor. That's a sound assumption because chances are you soon will be.

Picture the scene. Your loan officer glances up from reading your business plan and says, "You're assuming a vacancy rate of 6%." (That's the percentage of the year in which your units will be empty and generating no income because they're between tenancies.) "That sounds low to me," he continues. "How did you reach that number?" If you sit there, with your mouth opening and closing like a goldfish, you're dead in the water.

Instead, you need to have an instant response: I checked Apartment List's "Rental Vacancy Rates" page for my state or metropolitan area. And I added a bit to that to allow for the fact that my types of apartments have higher turnovers of tenants than some others. But I also spoke to two private landlords and two real estate agents who specialize in the local rental market. One said I should expect 5%, two said 6% and one said 7%. I felt 6% was sensible. But I did run the numbers on the basis of 7%. And I have that spreadsheet here ..."

You see? Assumptions aren't numbers you pluck from thin air. They're informed, intelligent projections. Of course, they may well turn out to be wrong. Unanticipated events (a recession, say) can and do intervene. But you must do all you can to be realistic.

Related: 8 Costs to Consider When Buying Rental Real Estate

Tips for landlords and partners

It's this high financial barrier to entry that forces many new landlords to enter partnerships with richer backers. Often they put up much or all of the money while you do the work.

Or you may prefer a straight loan to a partnership. Understand that "hard money" home loans typically require larger down payments and carry higher fees and interest rates.

A partnership can be a mutually beneficial, symbiotic relationship. Or one of you can end up feeling exploited and deeply unhappy.

So you need to come up with a formula for splitting the profits that rewards each of you appropriately. On the one hand, you must make an adequate living and have the prospect of future wealth. On the other, you need to recognize that new landlords are high-risk investments that demand significant returns.

You may be able to come up with a formula that sees your interest in the business grow as you reach certain, pre-agreed financial targets. And you might even negotiate an arrangement that sees the partner eventually exit the venture, once her money is returned along with an appropriately generous return.

You may think that a family member or close friend is your ideal partner. And you may be right. But remember you're then putting a precious relationship on the line. And familiarity can breed contempt, meaning a wholly professional relationship can sometimes be more successful.

Whomever you choose as your partner, consult with professionals before you sign an agreement or accept any money. If you have a cast-iron contract that clearly lays out the terms of the arrangement, there should be fewer opportunities for falling out later.

Top tips for landlords

That may be the top tip for landlords: recognize your own limitations and work around them. But there are others that rival that:

Learn quickly -- pick other landlords' brains. And be ready to share your knowledge when your turn comes

Get good at research -- to understand your marketplace, you need to complement advice from your fellow landlords and property professionals with solid data. Use free and occasionally paid-for online sources as well as local public records and the Census

Market precisely -- once you understand your pool of prospective tenants, you can work out how to reach them inexpensively. Online and word-of-mouth may be best. But sometimes you may benefit from signage, small ads or flyers

Network -- build relationships with local professionals and especially real estate agents. You want to be their first call when a bargain home comes onto the market

Pick tenants carefully -- It's unpleasant, time-consuming and expensive when you have to evict duds. Get good at picking winners. And use credit reports and background checks and take up references to weed out the worst. Oh, and social media can reveal a lot!

Observe the law -- Having a solid rental agreement or lease is just the start. You'll have to comply with laws and regulations over security and other deposits, eviction procedures, tenant privacy, chasing late rents, enforcing your rules -- and, of course, avoiding discriminatory practices when selecting tenants. You may need a lawyer on speed dial till you learn the ropes

Make mortgage payments your priority -- If you plan to expand your property business, you can't afford late payments. Being a perfect borrower is essential

How much money can you make?

Some of the biggest fortunes in America were built on real estate investments. But only by choosing the right investments. Experts say that investors who achieve an 8% to 10% COC (cash-on-cash) return are investing well.

To achieve the best returns, however, you may need to purchase properties that need a little work, invest in improvements and be more of a hand-on landlord. If you don't want to do that, buy Class-A properties and engage a property management company. That can be a sound strategy for those who don't go full-time as long as the property generates positive cash flow (makes a profit).

Millions of Americans are landlords. And most make a success of it. Follow the advice in this article to improve your chances of being one of the happy ones.